China & India Target Future GMP Manufacturing

China’s biological pipeline may take the lead

China and India have demonstrated their capability in good manufacturing practice (GMP) manufacture of small-molecule drugs for decades. But production of biological therapeutics has, until recently, not been done to GMP standards due to the greater complexity of bioproduction and the need for highly trained staff, regulatory expertise, and quality management systems. This is changing, and both India and China have moved their domestic bioproduction forward rapidly with the intent of challenging US and EU dominance. It is not likely a question of if, but rather when these regions, which include nearly 40% of the world’s population, will be manufacturing biologics for their domestic populations and global export as well.

Whether this happens in 5, 10, or 20 years, it is clear from our recent research that GMP export-quality biomanufacturing is in the sights of most biopharma facility managers in these regions. This article reviews our white paper research 1 ,2 comparing the Chinese and Indian biopharma industries’ perceptions of their efforts to globalize, what is yet missing, and when success will be achieved.

The domestic markets for biologics in these two countries represent a remarkable opportunity, and domestic biologics manufacturing is clearly important for both health policy and economic reasons. But the payoff may be seen in future export opportunities, and both countries are attempting to create positive investment climates to expedite domestic biomanufacturing capabilities so they can evolve their competence to permit export to more lucrative markets in Europe and North America. This, of course, will require manufacturing to GMP standards.

We recently queried professionals at bioprocessing facilities in China and India to identify their current capabilities and ambitions for the export of biological therapeutics. We interviewed 50 biopharmaceutical manufacturing executives in China and 104 executives in India. All were members of BioPlan Associates, Inc.’s Biotechnology Industry Council panel of regional and global bioprocessing experts. These surveys confirmed that both China and India are making efforts to become global bioprocessing centers.

Data about total biopharmaceutical manufacturing capacity (on-site bioreactor volume), drawn from BioPlan’s Top 1,000 Global Biopharmaceutical Facilities Index 3 and directory of Asian biomanufacturers, 4 show that India and China today have relatively comparable manufacturing capacities. Both countries also have a number of facilities owned by major Western biopharmaceutical companies. There are very significant differences, however. Chinese companies tend to be more oriented toward development and investment in innovative domestic products, for example, while Indian companies are investing in Western facilities and pursuing a more international strategy.

Findings China Vs India

In our research, we assessed critical areas where Chinese and Indian biomanufacturing executives recognize they lack capabilities required to participate globally. These executives clearly recognize their companies’ regional shortcomings and shared their perspectives on how they plan to move toward GMP export-quality bioprocessing.

Biopharmaceutical professionals in both countries believe they will achieve the required quality operations required by the United States, European Union, and other regions with stricter guidelines and enforcement of GMP, quality control, and documentation. In fact, nearly 90% of responding Chinese biologics managers indicated their companies plan to target global distribution of GMP-produced biologics within 10 years. Indian managers, in comparison, also recognize that they lack capabilities required to participate on the global stage. But among Indian biopharmaceutical professionals, 100% of biologics managers indicated their company plans to target global GMP production of biologics within 10 years.

Study respondents were asked to identify the top criteria for expanding their presence in global biopharmaceuticals. A country’s overall “quality image,” one of 17 tested in the survey, was deemed by almost 70% of Chinese survey respondents to be the most important criterion for competing globally in a GMP environment, with Chinese biopharmaceutical managers stating that overall quality image was a key weakness. Other criteria identified were:

- Overall quality image (68% selecting as a top attribute)

- More innovative biopharmaceutical pipeline (62%)

- Scientific/technical expertise (52%)

- Compliance track record/expertise (52%)

- 1BioPlan Associates, Inc. “China’s Advances in Global Biopharma and Bioprocessing: A 10-year Projection in Need for Innovation and Quality Improvements.” January 2017. http://www.bioplanassociates.com/

- 2BioPlan Associates, Inc. “India’s Advances in Global Biopharma and Bioprocessing: A 10-year Projection in Need for Innovation and Quality Improvements.” December 2016. http://www.bioplanassociates.com/

- 3BioPlan Associates, Inc. “BioPlan’s Top 1,000 Global Biopharmaceutical Facilities Index.” July 2017. http://www.top1000bio.com/

- 4BioPlan Associates, Inc. “Top 60 Biopharmaceutical Manufacturers in China.” March 2017. http://www.top1000bio.com/top60china/

| Category | Market size (USD) | Growth rate |

|---|---|---|

| Vaccines | $3.1 billion | 8.3% (from 2010–2014)* |

| mAbs | $0.42–$0.96 billion | 20.3%** |

| All biologicals | $6–8.5 billion | ~20%*** |

In comparison, fewer Indian than Chinese respondents—over 40%—perceived the country’s quality image to be a key weakness in its ability to compete globally. Although image was, again, a top attribute, it was noted by a lesser percentage:

- Overall quality image (41% selecting as a top-five attribute)

- Scientific/technical expertise (37%)

- Audit results (35%)

- Timeliness/scheduling/reliability (33%)

We also asked respondents what should be done to ensure their domestic industry develops the systems required for global-quality biomanufacturing. This question was intended to outline perception of what is needed to become competitive in a GMP environment.

In China, over three-quarters of respondents mentioned that having the ability to develop a more innovative biological product pipeline, with better R&D competence, will help establish global competitiveness within 10 years.

- Innovative biologics/better R&D (76%)

- Improve legal/regulatory compliance (44%)

- Better quality management systems (20%)

China’s pipeline development in recent years has shown rather rapid growth. In 2016 alone, the China Food and Drug Administration (CFDA) registered nearly 200 new biological pharmaceuticals entering clinical trials. BioPlan’s own analysis shows over 170 monoclonal antibody (mAb) therapeutics alone under clinical development in China, including a number of biosimilars: CD20, HER2, EGFR, VEGF, and TNF-alpha.

In India, over one-third of respondents stated that having the ability to develop marketable, innovative biological products tops the list of they need to help establish global competitiveness within 10 years. These prerequisites may be challenging to build from the ground up in India, given the relatively limited availability of biologics R&D expertise. Options for acquisition of these innovations may exist, however. Required core competencies identified by the Indian biopharmaceutical manufacturers included:

- Innovation/R&D product pipeline

- Production quality improvements

- Education, expertise, skills

- Regulatory expertise/audits

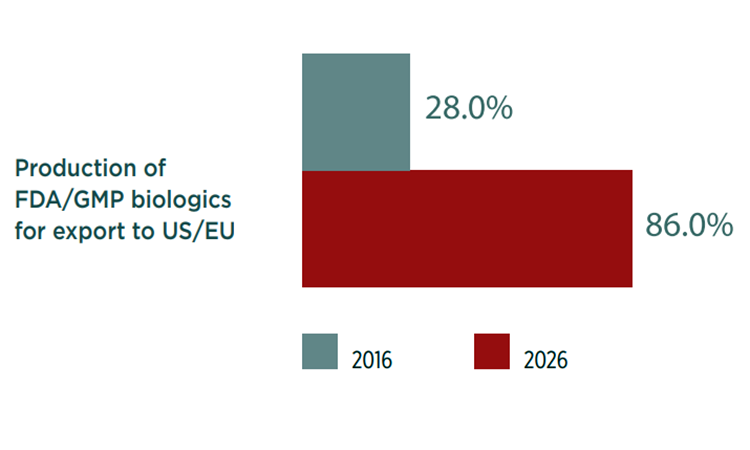

In our studies we asked respondents to indicate their facility’s primary objectives for biologics production today and in 10 years. In China today, 70% of biopharma facilities focus on production for domestic consumption. The Chinese biopharmaceutical industry is seeing relatively strong domestic demand as economic growth and expansion of national health insurance coverage creates demand. Multiple studies suggest the biological market in China will be the second-largest such market globally by 2020.

In 10 years, 86% of Chinese biopharma managers expect they will be focused on exporting to the United States and European Union. In other words, the great majority of Chinese biomanufacturers plan to produce biologics for both domestic and export consumption in 10 years (Figure 1).

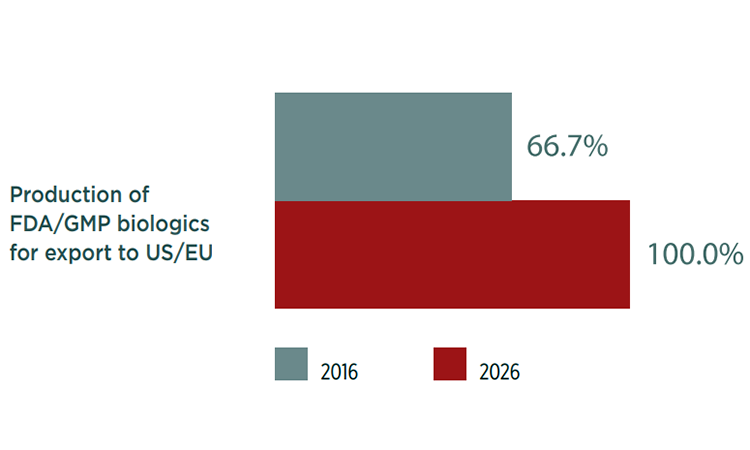

Indian respondents are also primarily focused on production for domestic consumption (81%) today. In 10 years, however, the focus will have shifted from domestic production to production for exports, particularly biosimilars. And 100% agreed they would also be focused on export production for US and EU markets (Figure 2).

Discussion

China appears to be better prepared for GMP export over the next 5 to 10 years. Chinese companies seem to be more oriented toward development of their own biological pipeline compared to India, perhaps due to bigger domestic market demand, government support, as well as more investment from the local venture capital industry. China’s pipeline development, especially in mAbs, shows strong growth potential for biological therapeutics.

Although China started rather late, it is making rapid progress. In 2014, the biological market in China was worth some $5 billion. According to Vincent Xie, former Director of CMC at Livzon mAbPharm, Inc., it is expected to grow to around $21 billion by 2020 at a compound annual growth rate of 20%.

Despite this, a major gap exists between China, the United States, and the European Union when it comes to prescribing mAbs as therapeutics. While mAbs are the largest class of biologics globally, they currently make up only 7% of the Chinese biologics market, according to IMS Health. The gap may be due to several factors:

- The price of imported mAbs can be prohibitive to many Chinese patients and the national health insurance does not currently cover many of them.

- A lack of lower-cost biosimilar mAbs from domestic drug makers is bottlenecking demand. Biosimilar and bio-better drugs from domestic drug makers are more likely to be listed in the national health insurance list and more affordable to Chinese clients.

Domestic companies are actively filing for clinical trials of mAbs in China. The Chinese market has strong demand for mAb products, but, at present, a large proportion of this demand is being filled by imports from developed countries. China imported $950 million worth of mAbs in the first half of 2015, according to estimates by Zhongkang CMH and others. Many domestic drug makers are working to seize this opportunity for future growth. Dr. Zhou Xinhua, CEO of Genor BioPharma, stated that with expanding national health insurance coverage and reimbursement rates, combined with the patent expiration of many mAbs developed by multinational companies, the mAb market in China will increase rapidly in the near future.

As noted above, the CFDA reports that close to 200 drug makers had submitted applications for mAb clinical trials to its investigational new drug (IND) application process by the end of 2015. It is estimated that over 600 drug makers in China are planning, at some level, to have therapeutic mAbs in the development pipeline. By the beginning of 2016, over 280 mAb clinical trial applications had been filed with the CFDA, according to Pharmacodia.com. Among these, were 132 from multinational companies with 148 from domestic drug makers.

Contract research organizations or contract manufacturing organizations (CMOs) involved in biologics are also targeting international clients, some of which have therapeutic mAb projects under development. Innovent Biologics is representative of this category. The most ambitious Chinese companies are already conducting clinical trials in regulated markets; Genor BioPharma, for example, has started phase 1 clinical study of its anti-HER2 mAb in Australia, and Teruisi Pharmaceutical, an antibody-therapeutics company founded by returnee scientists (Chinese scientists returning to China after working abroad), also plans to file an IND for one of its projects in the United States this year. We expect to see a more robust biological pipeline from Chinese companies in the near future.

Government and industry are working together to support the development of the Chinese biological pipeline. While we see the concern related directly to China’s limited R&D investments—especially insufficient investment in early-stage research on products and platforms—there have been signs in recent years of coordinated efforts to address the issue. In the past decade, China’s Ministry of Science and Technology has undertaken several projects, including the National Mega-Project for Innovative Drugs program, which funds development of biological pipelines from domestic companies. In 2016, Biodiscover.com reported a total of 32 biological products (from all but four domestic pharmaceutical companies) were in the last round of evaluation for the megaproject program, among them 18 mAbs, three vaccines, and two cell-therapy programs.

Regulatory authorities in China have also pursued reforms in recent years and are planning additional reforms that will facilitate growth of a more innovative biopharmaceutical industry. These reforms are intended to speed up the evaluation and approval process for more innovative therapeutics. Such reforms are essential if the industry is to shift from biogenerics to more innovative biopharmaceuticals.

China also initiated reforms in 2015 to remove the regulatory restrictions on contract manufacturing in the pharmaceutical industry, which mandated that drug developers must also be in charge of the manufacturing of the drug products they have developed. This is no longer the case country-wide with a trial marketing authorization holder program under which holders of drugs with CFDA drug-approval numbers are required to market and take the responsibility for the drug products while having the option to either manufacture them on their own or use contract manufacturers instead. This reform not only provides growth opportunities for CMOs but also makes it possible for biotech companies that are drug research-intensive but lacking in manufacturing infrastructure or expertise to focus on pipeline R&D, as they are no longer forced to spend significant resources to develop their own production facilities.

Local venture capital firms in China are also helping biotech company growth with pipeline development. This source of funding is relatively new. In the past, venture capital investors in China tended to shun biotech companies, since due to their limited exit options such investments were not easily sold or liquidated. BeiGene’s successful venture-capital-backed NASDAQ initial public offering and the first public offering in the United States by Hutchison Medi Pharma showed Chinese venture capital investors that exit can generate significant returns from biotech companies. Akeso Biopharma, an innovative biotechnology company founded in 2012 by a group of entrepreneurial returnees, for example, focuses on discovering and developing innovative biologics with international intellectual rights. The company got venture capital investment from Shenzhen Capital Group and CCB Principal Capital Asset Management Corporation and others in 2016 to develop a rich product pipeline targeting oncology plus autoimmune, inflammatory, and cardiovascular diseases. That same year, Qiming Ventures and Lilly Asia Venture invested in CanSinoBIO, a Tianjinbased biotech dedicated to developing an innovative vaccine pipeline. Analysts expect that exit routes via NASDAQ as well as China’s stock market (specifically the China’s Growth Enterprise Market) will attract more venture capital interest.

China’s ambition in GMP exports of biologics differs from India’s strategy of making investment overseas. As noted from our recent surveys, in 10 years 70% of Chinese biopharma facilities will focus on production for domestic consumption while the great majority, 86%, will be manufacturing for export to developed countries—a scenario made possible by China’s GMP regulations, updated in 2010, which demand higher manufacturing standards. In early 2017, the CFDA also announced plans to replace the current five-year GMP certification cycle by a dynamic unannounced inspection system. These moves are intended to bring China’s GMP code in line with European and American codes and regulations. Multinational pharmaceutical companies such as Boehringer Ingelheim and Pfizer Inc. are taking notice and have set up biologics manufacturing facilities in China. In fact, scarcely a month passes without a Chinese company announcing plans to build a biologics manufacturing center.4

India, in comparison, has long been home to many pharmaceutical companies that export small-molecule active pharmaceutical ingredients to regulated markets, but we do not find a similar trend for biologics. We are witnessing a reduction in foreign investment in India. At the same time, major Indian biopharmaceutical manufacturers are increasingly investing more overseas, often by expanding their manufacturing capacity and distribution networks in the United States and European Union, and by building new biopharmaceutical manufacturing facilities in other Asian countries. According to recent reports, Indian companies invested $1.5 billion in 2015 and more in 2016 in overseas facilities rather than investing in India’s domestic infrastructure. As an example, Aurobindo Pharma, which makes most of its drugs in India, is planning a second US facility. Its first US plant was established in August 2016, and the company will build a second sterile-injectables plant in New Jersey. In addition, due to increasing regulatory pressure from the FDA over quality problems in India, some companies are planning to enter the US market with US facilities and US-trained staff as it is seen as easier than trying to achieve the level of quality acceptable to the FDA in India.

Summary

Domestic demand in China and India for biopharmaceuticals has been growing, by various estimates, by between 15% and 20% annually, due to rising incomes, access to health care and insurance, and the availability of more products. Biopharma companies, especially those in China, are ramping up operations to serve emerging domestic markets, which will help develop the quality systems and competence required to enter Western markets. Biosimilars are beginning to play a role in India’s bio-industry development as several large companies now manufacture a handful of GMP-grade products approved in Western markets. In terms of profitability, however, a pipeline of biosimilars will not provide the same level of return that domestic innovative biologics would bring.

China continues to take steps toward aligning with global GMP requirements. However, China is not currently, and likely in the future will not be, among the lowest-cost destination countries for biopharmaceutical manufacturing. Our studies indicate that costs for the manufacture of typical mAb biosimilars in developing countries will continue to be higher than large-scale Big Pharma reference product facilities and typical new facilities coming online (e.g., Samsung and Celltrion in South Korea).

The Chinese biopharmaceutical industry appears to be investing in long-term global opportunities in biologics, including in bioproduction. With domestic Chinese manufacturers’ rational view of what the necessary investments in R&D, quality and regulatory systems, infrastructure, IP reform, health care, and workforce development will be within 10 to 20 years, it is likely China’s biologics may compete effectively in major markets, including the United States and Europe.